Rethinking Copper Tariffs

On July 9, 2025, President Trump announced the imposition of a sweeping 50 percent tariff on all imported copper, effective August 1. The announcement followed a five-month investigation under Section 232 of the Trade Expansion Act, through which the administration concluded that strengthening domestic copper production and reducing reliance on imports—including copper ore, scrap, and derivative products—is crucial to national security and that foreign reliance is undermining U.S. security interests.

Copper is indispensable to every pillar of U.S. security—national, economic, and energy-related. As the world’s second-largest consumer, the United States used approximately 1.6 million metric tons of refined copper in 2024. Yet, its participation in the global copper supply chain remains disproportionately small, contributing only 5.1 percent of mined copper and a mere 3.3 percent of refined output. This imbalance underscores the strategic vulnerability the tariffs aim to address and highlights the pressing need for a more resilient domestic copper ecosystem.

The United States urgently needs more copper to fuel its economic and technological ambitions. While traditional data centers require between 5,000 and 15,000 metric tons of copper, next-generation facilities built to support AI demand as much as 50,000 tons per site. Reflecting the scale of its ambitions, in April 2025, the Department of Energy announced the identification of 16 federal sites designated for AI and data center development—signaling a dramatic acceleration in infrastructure expansion.

After the tariff announcement, copper prices surged to an all-time high of $5.70 per pound—representing a 13 percent single-day increase and up 42 percent since the start of the year. Rising input costs are likely to drive up prices for a wide range of end-use goods, including electronics, consumer appliances, construction materials, automobiles, and electrical infrastructure.

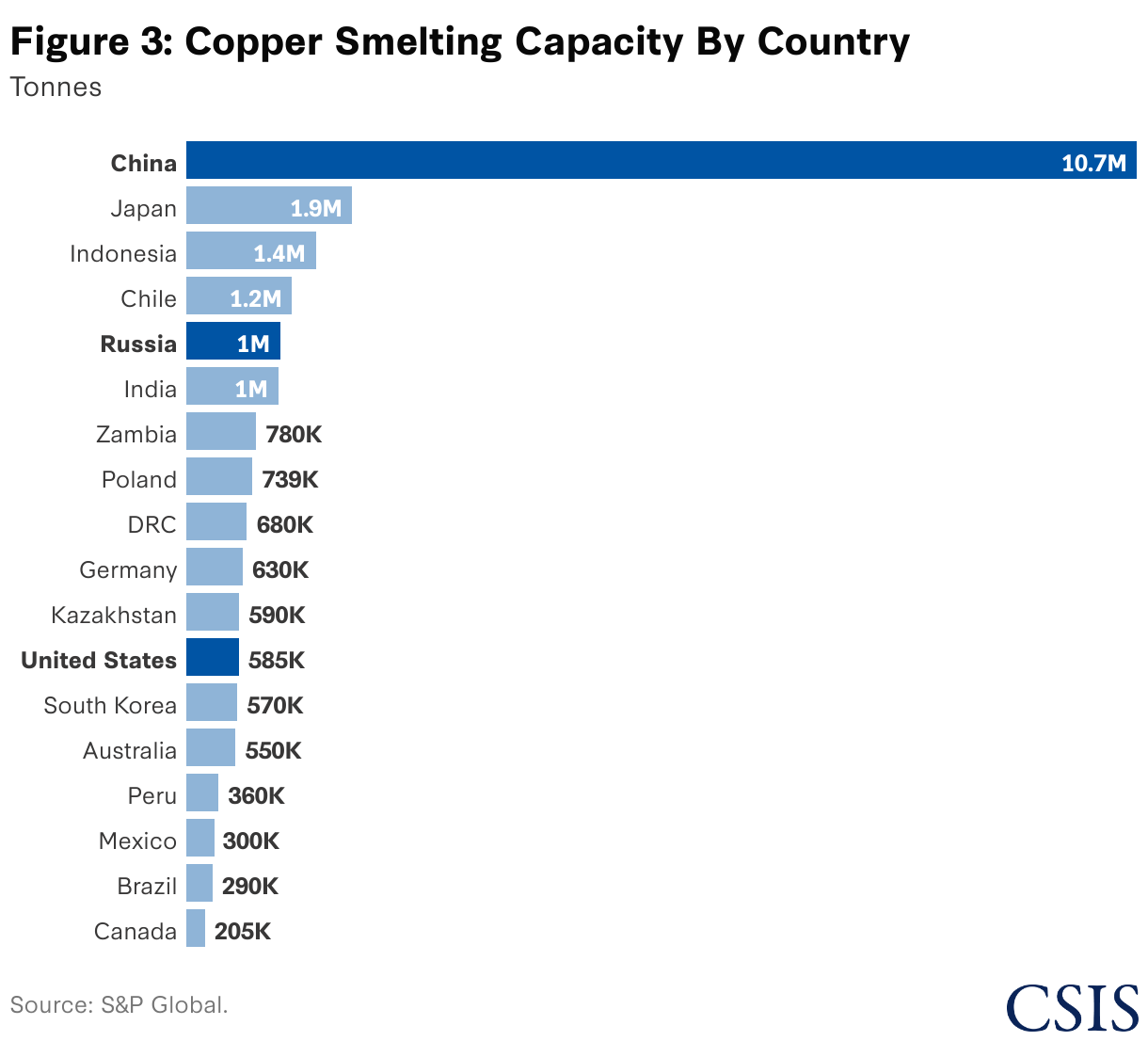

While the tariffs are designed to incentivize domestic capabilities, they remain limited—particularly in the midstream segment of the supply chain. In 2024, the United States produced 1.2 million metric tons of mined copper, primarily from operations in Arizona, Utah, and Nevada. Despite this substantial output, the United States only has 585,000 metric tons of domestic smelting capacity—just half of what it mines. Thus, a large share must be exported for processing, underscoring a critical gap in the supply chain. The majority of U.S. copper ores and concentrates were shipped to Mexico (27 percent), Canada (23 percent), Japan (22 percent), and China (18 percent), leaving U.S. producers reliant on foreign smelters to complete the value chain.

Challenges with Developing the U.S. Copper Supply Chain

In 2024, the United States consumed 1.6 million tons of copper but produced only 1.2 million tons and smelted just 585,000 tons—demonstrating that it falls short of self-sufficiency in both production and processing. While strengthening domestic capabilities is critical for national security, several significant obstacles remain.

First, copper production in the United States is characterized by relatively high costs. The average total cash cost of production of 405 copper mines worldwide is $2.04 per pound. In contrast, the average for U.S. mines stood at $2.65 per pound. Among the 100 most cost-competitive mines globally—ranked by total cash cost per pound—only one is in the United States. The country’s largest operating copper mine, Morenci, reported a total cash cost of $3.16 per pound, highlighting the broader cost challenges faced by the domestic industry.

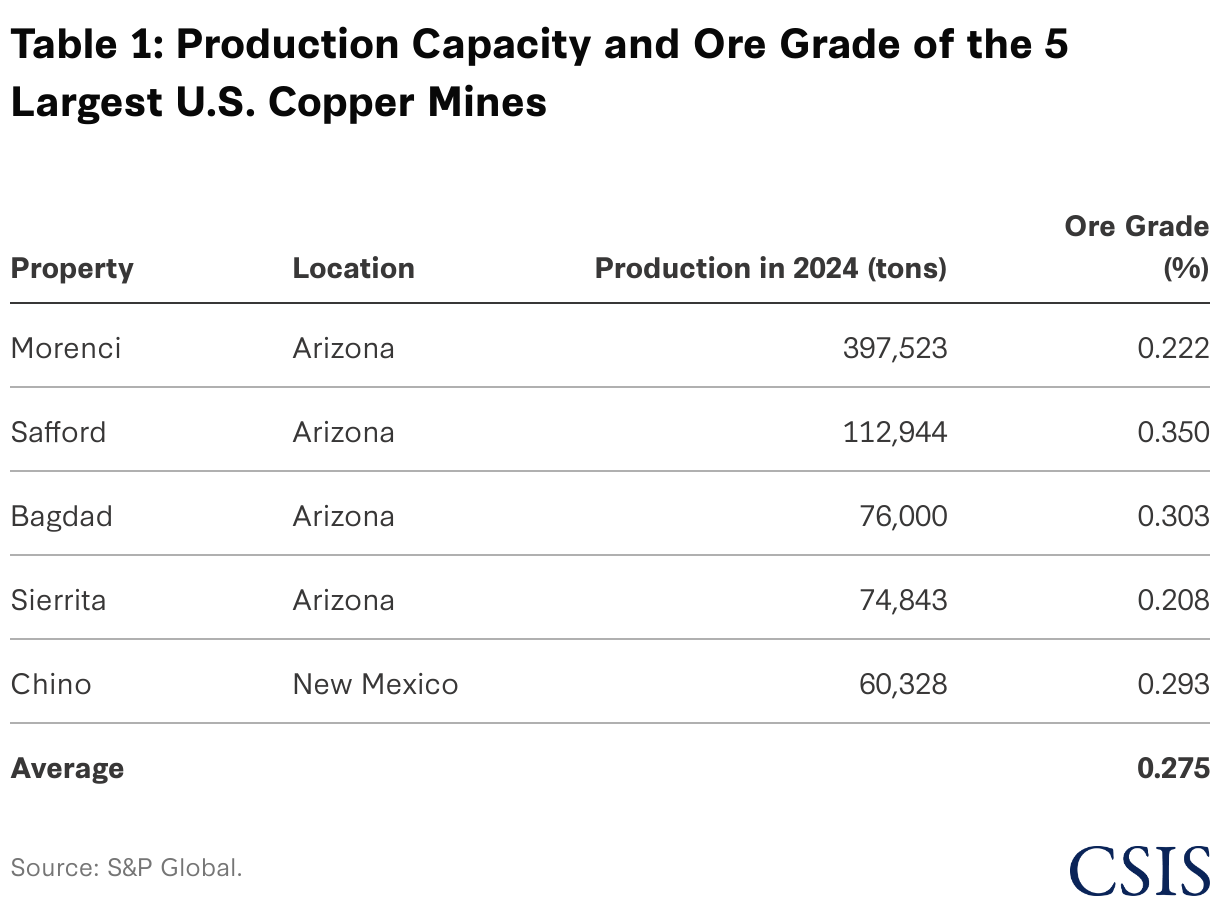

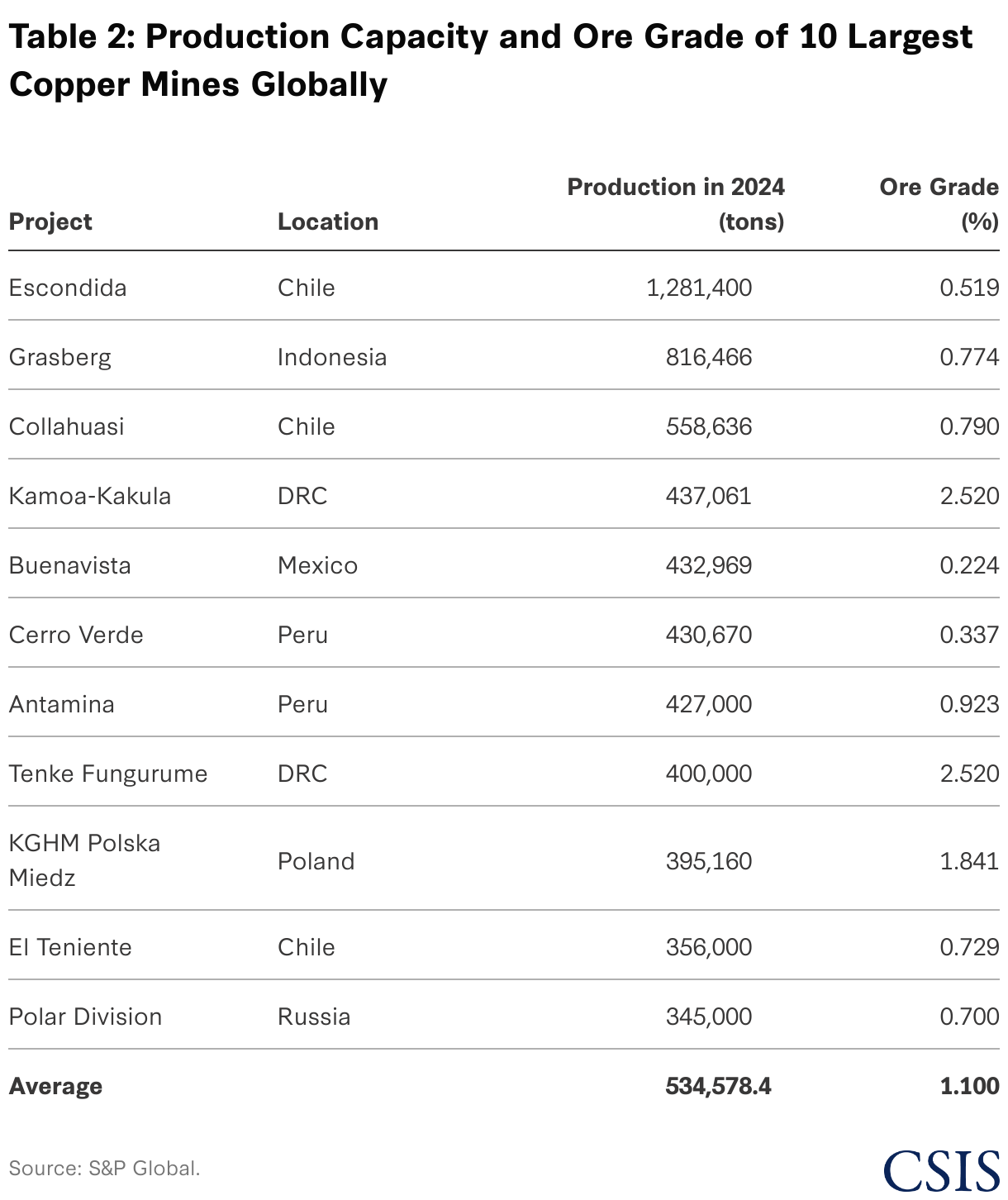

Second, copper ore grades in the United States are low. When looking at the five largest operating copper mines in the United States—which account for two-thirds of U.S. copper production—the average ore grade is just 0.3 percent. In comparison, the average ore grade of the 10 largest operating copper mines in the world—located in the Democratic Republic of Congo (DRC), Poland, Chile, Indonesia, Russia, Australia, and Mongolia—was 1.1 percent, which is nearly four times the average of the United States.

Third, there are only two smelters in the United States, and the economics of developing new smelters do not add up right now. In 2025, smelting charges—the fees smelters earn for processing copper concentrate—fell to a historic low of $45 per ton. At these levels, smelters are effectively operating at a loss, continuing production solely to maintain plant functionality. Reflecting these unfavorable market conditions, Glencore suspended operations at its Philippine Associated Smelting and Refining copper smelter in the Philippines. Industry analysts warn that refining charges could turn negative for the first time, underscoring the severe economic pressures currently facing the global copper smelting sector.

While tariffs could, in theory, enhance the attractiveness of developing domestic smelting capacity, copper smelters require substantial capital investment and long lead times. For example, U.S.-based Freeport-McMoRan invested roughly $4 billion and spent nearly five years constructing its Grasberg smelter in Indonesia (though 8–9 years with planning lead time).

Replicating such a project in the United States would likely entail significantly higher costs, driven in large part by higher labor costs. Given the razor-thin and/or negative profit margins of copper smelting, firms would require ongoing financial support for operating costs. To exacerbate this, confidence in the stability of tariff policies has also eroded investor sentiment on building an additional smelter.

Potential Consequences of Tariffs

The United States relies on imports to meet approximately 50 percent of its copper consumption. The majority of its refined copper imports originate from Chile (65 percent), followed by Canada (17 percent), Mexico (9 percent), and Peru (6 percent). Each of these supplier countries would be directly affected by the proposed tariffs, with potential implications for both supply chain stability and domestic pricing.

Risk of Market Diversion

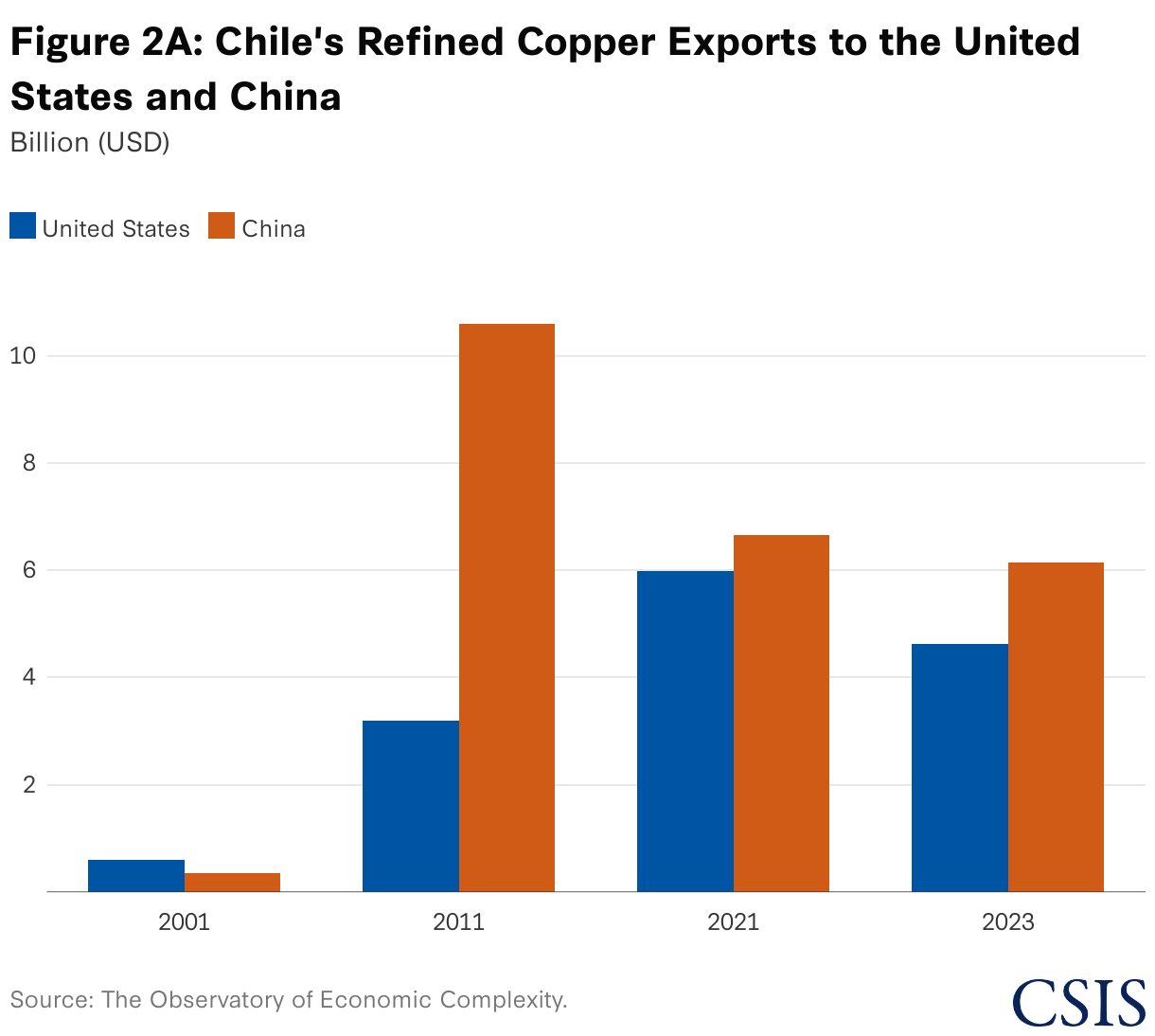

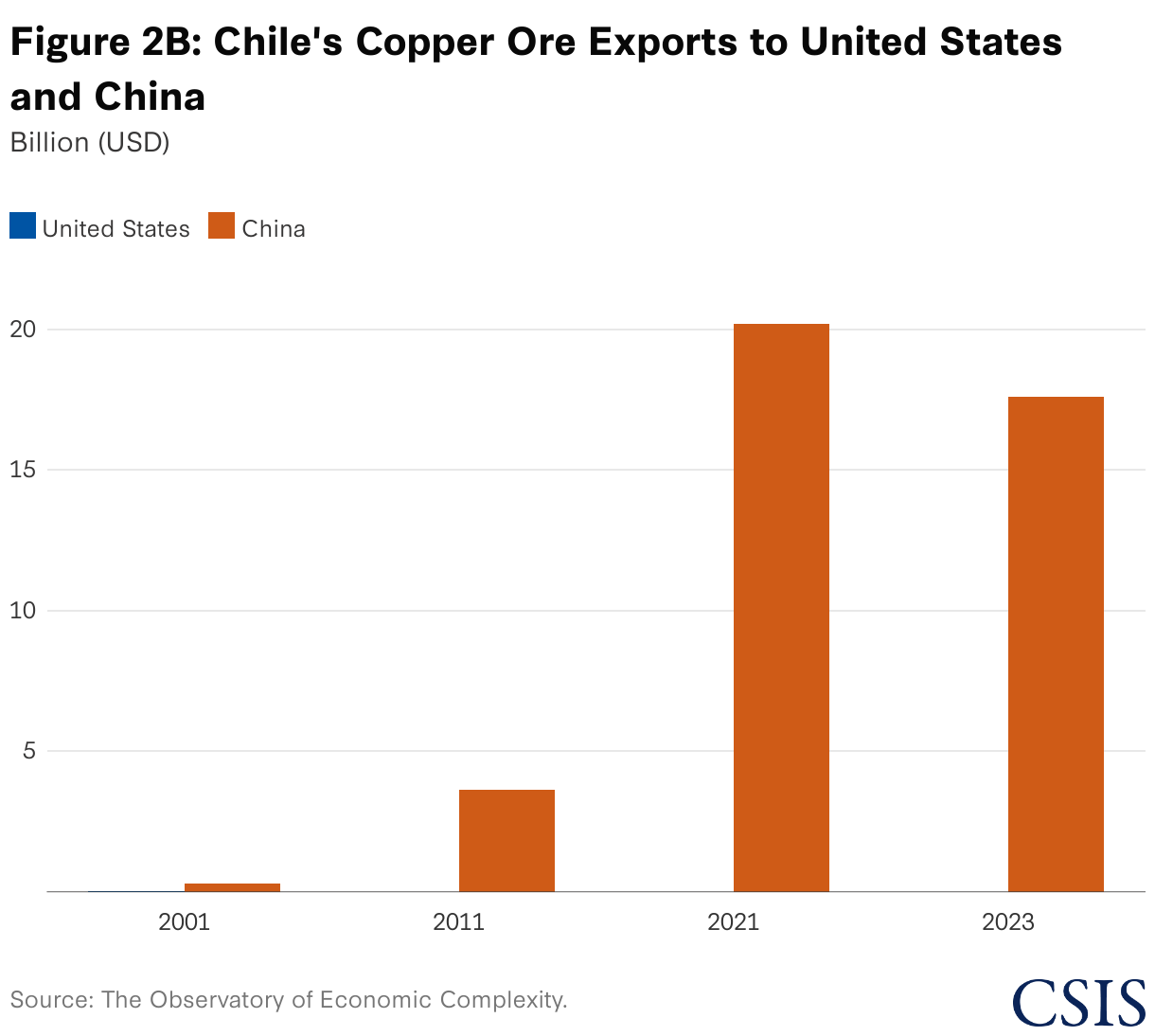

There is a significant risk that copper-exporting countries will redirect shipments to China in response to U.S. tariffs. Chile and Mexico have already indicated they may seek markets elsewhere to avoid the tariffs. This will accelerate a competition the United States is already losing in these countries. This shift would accelerate a broader trend in which the United States is already losing strategic economic influence. In 2001, Chile exported nearly equal values of copper to the United States and China—$0.63 billion and $0.62 billion, respectively. By 2023, Chile sent $17.5 billion in copper ore and $6.2 billion in refined copper to China, while the United States imported $4.6 billion in refined copper and no copper ore. The United States’ position has already been weakened: Chile’s refined copper exports to the United States fell by nearly 33 percent between 2021 and 2023.

Canada is the United States’ second biggest copper supplier. In 2023, it sent 96.8 percent of the $1.26 billion in copper it exported to the United States. Tariffs on Canada could displace Canadian copper exports. Given the global outlook for copper demand growth—which could see demand increase 70 percent by 2050 from 30 million tons to 50 million tons annually—there will be no shortage of alternative markets eager to secure refined Canadian copper.

Risk of Production Stoppages

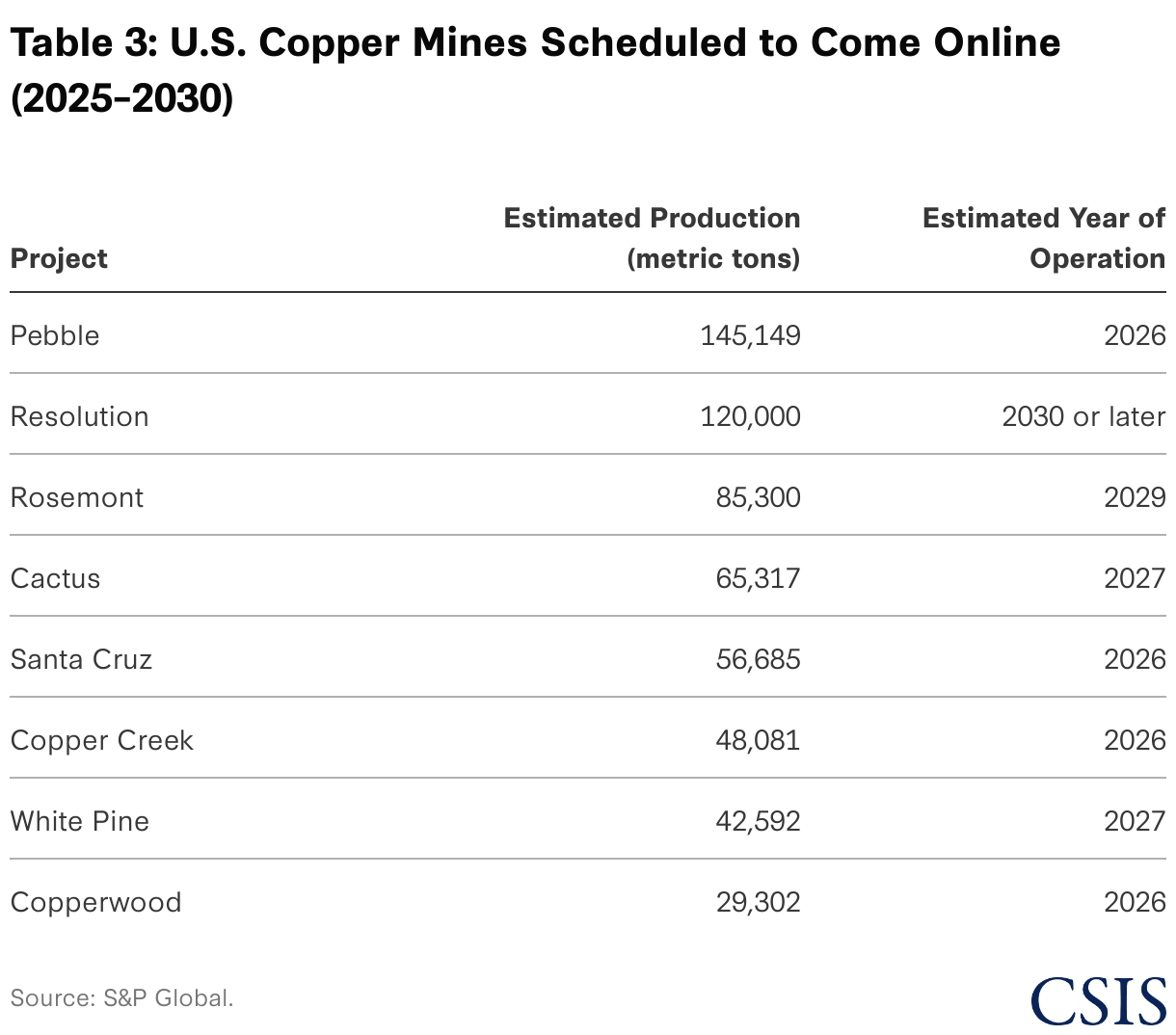

U.S. copper ore production is on track to rise in coming years as new projects come online under the Trump administration’s expedited permitting regime. By 2030, U.S. copper production is forecasted to grow 50 percent with the addition of major projects like the Pebble Mine in Alaska and the Resolution Copper project in Arizona. For years, these projects were tied up in complicated legal battles, contested land transfers, and permitting bottlenecks. Now, the Trump administration is expediting these kinds of mining projects. In April 2025, the Trump administration is actively prioritizing Resolution Copper as a Federal Permitting Improvement Steering Council “transparency project” selected to fast-track permitting and facilitate land transfer.

However, due to the high costs, long lead times, and limited commercial viability of building new copper smelters in the United States, a significant portion of copper concentrate must be exported for processing before returning for downstream manufacturing. Proposed 50 percent tariffs jeopardize this arrangement, risking disruptions to cross-border trade.

Indonesia offers a cautionary example of the risks associated with abrupt policy shifts. In 2014, U.S.-based Newmont was forced to suspend copper production at its Batu Hijau mine after stockpiles reached capacity due to an export ban. The Indonesian government compounded the pressure by introducing escalating export duties on copper concentrate to enforce compliance with new domestic processing mandates. Despite efforts to negotiate a compromise that would preserve the commercial viability of its operations and amid mounting demands to meet foreign ownership divestment requirements, Newmont ultimately chose to divest its assets and exit Indonesia in 2016.

Recommendations

1. Adopt a product-specific tariff structure for the copper supply chain: To minimize market distortions and adverse downstream consequences, a more calibrated, product-specific tariff structure is essential to preserving supply chain resilience while encouraging strategic investment in domestic processing capacity.

Nearly 80 percent of global copper mining results in the production of copper concentrate, which must then be processed through smelting and refining to produce copper cathode, which is the form traded on markets like the London Metal Exchange. Copper cathode, along with high-quality recycled scrap, is subsequently purchased by semi-fabricators, who convert it into intermediate products such as wire rod, tubes, plates, and sheets. These materials serve as the foundational inputs for the manufacturing of finished goods across a wide range of industries.

When looking at the upstream segment of the supply chain, imposing tariffs on copper ore is unlikely to significantly impact markets—the United States already produces more copper ore than it can process. Thus, other countries will not send copper to the United States, irrespective of the tariff rate. On the other hand, when looking at refined copper, tariffs on copper cathode could be highly damaging to domestic manufacturing. Until the United States has increased domestic smelting and refining capacity, the downstream impacts of the tariffs will jeopardize the U.S. economic growth agenda. And finally, when looking at the downstream segment of the supply chain, a moderate tariff rate on semi-fabricated goods could incentivize a domestic manufacturing industry, which is an easier industry to develop. A one-size-fits-all approach risks undermining these critical industries and could ultimately reduce the competitiveness of the broader U.S. economy.

2. Eliminate tariffs with strategic allies: Allies play a critical role in supporting secure and resilient copper supply chains by providing smelting and refining capacity to complement U.S. ore production. Normalizing trade relations with strategic partners is necessary to stabilize copper supply chains. At present, the United States’ processing capabilities amount to just 52.4 percent of its annual production. While new mines will increase production capabilities, no smelters will come online in the near term, exacerbating the disparity between production and processing capabilities. Thus, even as the United States ramps up production, it will need to lean into allies to smelt. For example, India’s Kutch Copper facility in Mundra, Gujarat, is set to become the world’s largest single-site copper smelting complex, with an initial annual capacity of 500,000 metric tons. Creating a favorable tariff regime with non-adversarial countries will be crucial.

· North American allies: Canada and Mexico are indispensable North American partners, purchasing 50 percent of the U.S. copper ore exports and, in return, supplying the U.S. with 26 percent of its refined copper imports. In Canada, Glencore operates the country’s sole copper smelter, which processes feedstock sourced from both Canadian and U.S. mines. Similarly, Mexico accepts U.S. copper concentrate at its La Caridad facility. Southern Copper’s $1 billion investment in the Empalme smelter and refinery—now entering preproduction—will nearly double Mexico’s processing capacity, creating an opportunity to accommodate additional U.S. feedstock as new mines come online. Implementing tariff exemptions for these North American partners would strengthen regional copper supply chains while helping to stabilize prices for U.S. consumers.

· Strategic Free Trade Agreement (FTA) allies: The majority of the United States’ refined copper imports originate from Chile (65 percent), with Peru accounting for a smaller share (6 percent). Honoring the FTA and eliminating copper tariffs will be crucial to ensuring there is no trade diversion or supply chain disruptions. In the longer term, if the United States builds domestic copper smelting capabilities, Chile and Peru could also be important sources of ore.

· Strategic new partners: attracting new investment in countries prioritized for bilateral minerals cooperation with the United States will be challenging with steep tariffs. For instance, the DRC, the world’s third-largest copper producer and a key partner in an anticipated U.S. minerals cooperation agreement, faces headwinds. Cobalt and copper are co-mined in the DRC’s ore bodies. While copper remains commercially attractive, cobalt prices have declined by more than 60 percent over the past two years, significantly reducing the overall profitability of mining operations. This cobalt pricing dynamic, coupled with copper tariffs, may deter new investment despite ongoing diplomatic and strategic engagement.

3. Develop incentives for domestic midstream capacity: The Trump administration’s approach to strengthening the domestic minerals ecosystem has primarily focused on accelerating permitting processes and facilitating land transfers. However, the use of targeted tax credits and financial incentives to bolster midstream processing is essential. When the Inflation Reduction Act was enacted in 2022, copper was excluded from eligibility under the Section 45X production tax credit, as it was not listed as a critical mineral by the U.S. Geological Survey. Although Section 45X is now being phased out, the establishment of a new incentive mechanism, particularly a production tax credit, should be considered to enhance the commercial viability of copper processing and support the development of a robust domestic supply chain.

4. Leverage government equity and a price floor: Attracting private capital into copper processing is difficult—profit margins are tight, permitting barriers are high, and volatile prices create new risks. As a result, the U.S. government will need to provide a new support model, blending government equity with private financing, to develop domestic copper smelting capacity as a strategic priority.

This model has already been initiated for domestic rare earths processing. Since China imposed heavy rare earth export restrictions in April 2025, the U.S. government accelerated efforts to create a more secure mine-to-magnet supply chain. In July 2025, the U.S. Department of Defense (DOD) announced a partnership with U.S. rare earths producer MP Materials Corp. The DOD will purchase $400 million in preferred stock to become the largest shareholder in the largest domestic rare earths producer. The partnership also includes $150 million in concessional financing, a price floor of $110 (nearly double current market prices), and guaranteed DOD offtake of domestically produced rare earth magnets.

A similar approach could substantially reduce the risks associated with developing domestic copper smelting capacity by enabling the U.S. government to make a strategic equity investment in a smelter operated by a U.S.-based firm or consortium of U.S. firms. Additionally, considering persistently low—and potentially negative—refining charges, the establishment of a price floor would serve as a critical safeguard, providing the industry with protection against market volatility and enhancing the commercial viability of domestic processing operations.